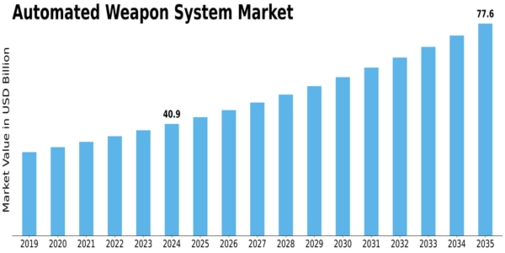

With the Automated Weapon System Market poised to grow from USD 41.58 billion in 2024 to USD 77.64 billion by 2035 at a 5.84% CAGR (per MRFR) , companies operating in this domain must adopt strategic planning to capture value and lead in a complex defence ecosystem.

Industry Overview

The automated weapon system sector spans a range of technologies—from unmanned aerial vehicles and robotics to sensors, command & control and cloud-enabled deployment. Market growth is closely tied to defence modernisation, technological innovation, geopolitical tensions and procurement budgets.

Market Outlook

The long-term horizon to 2035 signals sustained demand. A CAGR of 5.84% is moderate, so strategic consistency, rather than short-term bursts, will define winners. The market’s volume (USD 77.64 billion by 2035) indicates compelling scale for those aligned with defence strategies.

Segmentation Growth & Strategic Implications

The MRFR segmentation data reveals priority areas for strategy:

- Type: With land systems dominant and aerial systems growing fastest, companies should maintain capability in ground platforms while expanding UAV/autonomous aerial offerings.

- Component: As sensors represent the fastest‐growing component, building sensor-fusion and AI/ML capabilities is strategically advantageous.

- Deployment Mode: On-premises will continue to dominate, but cloud-based systems are gaining. Firms should plan for hybrid models and secure cloud offerings.

- End-User & Region: Military end-user remains key; but contractors and governments beyond traditional buyers are expanding. Regionally, North America remains large; Asia-Pacific offers fastest growth.

Key Players & Competitive Strategy

The MRFR list of key players (Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, General Dynamics, Thales Group, Leonardo, Elbit Systems, Saab) reflects the incumbency in this market. Strategic planning for newer entrants or adjacent-technology firms should focus on:

- Developing niche capabilities (e.g., AI/ML, sensors, unmanned platforms) that complement major contractors.

- Partnering or forming alliances with incumbents to access defence procurement channels.

- Targeting emerging regions (APAC, MEA) for geographic expansion.

- Monitoring regulatory/ethical developments, since autonomous weapon systems are sensitive and may face future constraints.

Final Thoughts

In a Automated Weapon System Market forecast to approach USD 77.64 billion by 2035, success will not come merely from entering the space—but from executing strategically: aligning with growth segments (aerial systems, sensors, cloud/hybrid deployment), understanding regional dynamics, forming strong partnerships, and navigating regulatory frameworks. For companies that plan accordingly, this market offers long-term value and competitive differentiation.

Related Report:

Airport Passenger Screening Systems Market

Air Cargo Security Screening Market